INTRODUCTION

Budgeting is one of the most important issues in management accounting (Frucot & White, 2006;Lau & Tan, 2012;Maiga & Jacobs, 2007). For several decades, research into participation in budgeting shows a significant involvement by management (Agbejule & Saarikoski, 2006;Brownell & Dunk, 1991;Frucot & White, 2006;Jermias & Yigit, 2013;Lau & Lim, 2002;Leach-López, Stammerjohan, & Lee, 2009;Leach-López, Stammerjohan, & McNair, 2007;Uyar & Bilgin, 2011;Yuliansyah & Khan, 2017). However, until now the findings of research into the relationship between participation in budgeting, on the one hand, and performance, on the other hand, are inconsistent and cannot be generalised to different settings (Derfuss, 2016;Maiga, 2005;Yuen, 2006,2007). For example,Derfuss (2016) claims that ‘The relationship of participative budgeting with performance presents a much debated but still unsettled issue in management accounting research.’ Another writer goes further than “unsettled”. They say bluntly that ‘empirical findings regarding the direct association between budget participation and performance have proved the influence to be wildly variable, ranging from strongly positive [...] to weak [...] to non existent [...] and even negative[...]’ ((Maiga, 2005, p. 212).

Based on these arguments,Yuen (2007, p. 534) says that ‘These mixed results indicate that no simple relationship exists between budgetary participation and job performance, and suggest that there could be other variables involved’.

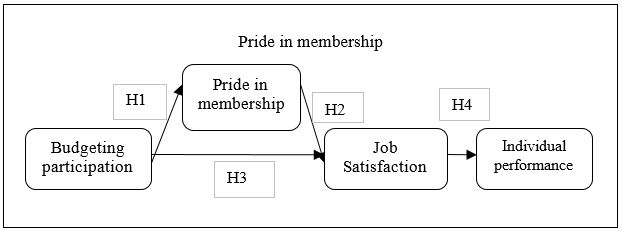

Thus, the aim of this study is to investigate the relationship between participation in budgeting and job performance with two other variables pride in membership and job satisfaction pride in membership and job satisfaction involved in different settings.

Most research on participation in budgeting comes from western countries and from North America. Unlike previous studies, this one is Asian, specifically in Lombok, already Indonesia’s second biggest tourism destination after Bali. As for hospitality, “the [...] industry is one of the most important service industries’ (Uyar & Bilgin, 2011). People involved in budgeting make better decisions generally (Groen, Wouters, & Wilderom, 2012). Psychologists suggest that such people gain more individual job satisfaction (Boujelbene & Affes, 2012;Stammerjohan, Leach, & Stammerjohan, 2015), while satisfaction itself enhances job performance. However, accountants rarely investigate the links between budgetary participation, individual pride as a member of an organisation, job satisfaction, and individual performance – that is, subordinates’ performance.

Pride in organisational membership, notablythe result of self-identification with a company that has a good reputation and record, (Mischkind, 1998), develops further when both extrinsic and intrinsic factors motivate employees (Bouckaert, 2001;Helm, 2013), increasing job satisfaction (Helm, 2013). In the hotel industry, good or bad service has many facets (Darvishmotevali, Arasli, & Kilic, 2017); including cycles of internal service quality, a concept affirmed by many scholars (Brady & Cronin Jr, 2001;Heskett, Jones, Loveman, Sasser Jr, & Schlesinger, 1994;Newman, 2001;Roth & Van Der Velde, 1991;Schlesinger & Heskett, 1991a)..Unless employees are happy, it is quite difficult for an organisation to provide good service to its customers (Gouthier & Rhein, 2011). Job satisfaction, therefore, is an organization’s responsibility: it motivates the worker’s performance (Jermias & Setiawan, 2008).

It follows from the above that this is our research question: Does the extent to which pride in membership has a role as a result of participation in decision making improve individual performance through job satisfaction?

Previous studies in management accounting do not investigate the role of participation in budgeting in fostering pride in membership which itself increases job satisfaction and ultimately increases individual performance. We study, as we said, the hotel industry in Lombok, the second biggest tourism destination in Indonesia after Bali. The government of Nusa Tenggara Barat province in Lombok actively promotes tourism to increase provincial revenue.

This study contributes in several ways. Firstly, following up the idea ofLau (2015)that budgeting participation influences all three variables pride in membership, job satisfaction, and individual performance we discover that it is not discussed anywhere, as far as we can see, within a single integrated and comprehensive model. Thus, our present study provides a contribution to the management accounting literature by incorporating pride in membership and job satisfaction as mediating aspects in a model both comprehensive and integrated.

Secondly, although budgeting is well documented in manufacturing, it is not so in the service sector, particularly in hospitality (Haktanir & Harris, 2005;Mia & Patiar, 2001). The writersClaver-Cortés, Pereira-Moliner, José Tarí, and Molina-Azorín (2008, p. 229) suggest that ‘more research on such issues is needed to fill this gap […] in the hotel industry.’

Thirdly, we extend the conceptual framework. Many people study individual performance at the managerial level (see:Derfuss, 2016). We, however, make a point of investigating lower-level employees and we show that budgeting improves performance at that level. We focus on lower-level employees or subordinate employees for two reasons: 1) because many studies of budgeting participation are conducted at the managerial level, and we expect that analysis of lower level individuals might have a different and more generalisable result (Frucot & White, 2006); and 2)Chong, Eggleton, and Leong (2005, p. 214)’s claim that ‘no studies have explicitly tested its [PIM’s] impact on subordinates’ job performance, and its potential influence within a cognitive model of budgetary participation’. leads us to consider the pride in membership as a variable which is a link between the variables participation in budgeting and job satisfaction . To the best of our knowledge, this approach is unique. We believe that by adding pride in membership as a mediating variable we enrich the field of study of management accounting.

The remainder of this paper is structured into four main sections: Section 1 reviews the literature and develops our hypotheses. Section 2 explains the research methods. Section 3 analyses the data and tests the hypotheses. In section 4 we present our conclusions and suggest areas for future research.

1. LITERATURE REVIEW

Budgeting is crucial to organisational achievement (Huang & Chen, 2010;Kung, Huang, & Cheng, 2013). Scholars argue that participation in budgeting improves communication, increases job satisfaction and improves performance (Jermias & Setiawan, 2008). However, there is a possibility that participation may be a mediating variable, perhaps with a psychological component (Lau & Tan, 2012).A person involved in the budgeting process feels more valued as a member of the organisation, according to psychologists (Kung et al., 2013). This is bond that leads to work satisfaction and better performance (Huang & Chen, 2010;Jermias & Setiawan, 2008;Lau & Tan, 2003;Yuliansyah & Khan, 2017).

In addition, job satisfaction may also be influenced by how well superiors maintain open communication channels with their subordinates, and to what extent the superiors foster a two-way flow of information about budgeting and decision making throughout the organisation. Superiors who encourage subordinates’ involvement in budgetary forecasts are perceived as trustworty persons (Yuliansyah & Khan, 2017). This process will increase an individual’s job satisfaction. As far as internal motivation to provide quality service is concerned, when an individual has a higher level of job satisfaction , they put more effort into providing service of high quality, and that effort leads to the improvement of performance – at least as seen by the consumer, who may value the effort more highly than the putative result, if any (Heskett et al., 1994;Heskett, Jones, Loveman, Sasser Jr, & Schlesinger, 2008;Reichheld & Sasser Jr, 1990; see:Schlesinger & Heskett, 1991b).

In contrast, lack of individual participation in company decisions, of which budgeting is our chosen prime example, decreases individual job satisfaction and in turn affects employee commitment. (Steven et al., 2013). Consequently, we expect a lower level of individual performance. Once more, “ when superiors allow subordinates to participate in decision making, that process gives individuals more pride, more self- actualization, and eventually more job satisfaction ” (Kim et al., 2017). All positive factors lead to the increase of individual performance. Hence, in accordance with the above exposition, we propose the following research framework:

1.1. Budgeting Participation and Pride in Membership

Although previous studies are more often found in the field of psychology than in management accounting, we discover a positive relationship between these two variables: budgeting participation and PIM. According to psychological theoristsDecrop & Derbaix (2010) andKraemer, Gouthier, & Heidenreich (2017), pride in an individual is stimulated by the feeling of satisfaction they get as they perform well within an organisation. This feeling of satisfaction is not once-only, but it happens repeatedly (Gouthier & Rhein, 2011). It is influenced by many factors. For exampleYuliansyah, Bui, & Mohamed (2016a) note that individual job satisfaction increases as the individual is valued fairly.

In addition,Yuliansyah & Khan’s study (2017) in the public sector shows that budgeting participation increases individual self-efficacy, as employees are trusted by managers to contribute ideas and make suggestions of what to do to help the organisation. Since they are trusted and their voice is heard, an employee feels more pride in themself and their organisation (Ni, Su, Chung, & Cheng, 2009). We argue here that budgeting participation has a positive effect on pride in membership– hypothesis H1.

H1. Budgeting participation has a positive effect on pride in membership

1.2. Pride in Membership and Job Satisfaction

Kraemer, Gouthier, and Heidenreich (2017) state that pride in membership increases when an organisation acknowledges an individual’s better performance compared to others within the organisation. In addition,Yuliansyah, Bui, and Mohamed (2016)’s study in the banking sector finds that appropriate performance measurement increases pride in membership because achievement is fairly valued. Since pride in individual achievement stimulates individual job satisfaction, the organisation is better off as employees strive to do better (Gouthier & Rhein, 2011).

An example can be taken fromHelm (2013). Their cross-sectional survey of 439 employees in different industries shows that pride in membership has a positive influence on job satisfaction . In addition,Helm (2013) notes that the individual who does better and get rewards from an organisation becomes more committed to it. Similarly, three-wave panel data of frontline employees taken from various industries byKraemer et al. (2017) confirms the positive effect over time, andMorrison (1997) adds that job satisfaction has a positive effect on the desire of the employee to stay working at the company. We predict that the desire to continue in an organisation depends on PIM, hence hypothesis H2:

H2. Pride in Membership has a positive effect on Job Satisfaction.

1.3. Budgeting Participation and Job Satisfaction

Some studies find a positive relationship between budgetary participation in decision making and job satisfaction. Allowing a subordinate to participate in decision making increases their self-esteem and their job satisfaction (Chong, Eggleton, & Leong, 2006). In addition, according to psychologist Shields & Shields (Shields & Shields, 1998, p. 59) budgeting participation enhances individual job satisfaction ‘because the process (act) of participation allows a subordinate to experience self respect and feelings of equality arising from the opportunity to express their values.’

When employees participate directly in the budgetary process, it necessarily follows that they understand better the problems of implementation.Chong et al. (2005) say that participation in budgeting makes corporate success more likely, which in turn enhances an individual’s job satisfaction. Participation allows better communication, interaction, and cooperation (Yuliansyah & Khan, 2017), all with a positive effect. At the simplest level, studies show that there are positive effects from budgeting participation (Chong et al., 2005,2006). Hence our H3:

H3. Budgeting Participation has a positive effect on Job Satisfaction

1.4. Job Satisfaction and Individual performance

Job satisfaction and individual performance attract much attention in the literature, and have done so for a long time. Job satisfaction as defined byLocke (1976, p. 1300) is ‘a pleasurable or positive emotional state resulting from the appraisal of one’s job or job experience’.Strauss (1968, p. 264) concludes that ‘higher morale [...] leads to improved productivity’. That is, people with high morale will work more seriously and give higher performance. (Olsen et al., 2007).Chong et al. (2006, p. 74) say that ‘subordinates who are highly satisfied with their job, are more likely to exert additional effort to perform’.Cullen, Edwards, Casper, and Gue (2014) point out that job satisfaction follows from perceived organizational support. When an organization supports – or even recognises – individual activities, individual satisfaction boosts performance.

Yuliansyah, Bui, et al. (2016) andJudge, Thoresen, Bono, & Patton (2001) agree that the relationship is reciprocal. It means that job satisfaction stems from appropriate evaluation of individual performance and that satisfaction itself triggers harder work (Atkinson, Waterhouse, & Wells, 1997;Heskett et al., 1994;Schlesinger & Heskett, 1991a;Zeithaml, Berry, & Parasuraman, 1988). A survey byFu and Deshpande (2014) of 476 insurance employees in China finds again that job satisfaction improves organisational commitment and individual performance. In addition a survey study undertaken byChong et al. (2006) in Australian financial services sector has the same outcome. Thus, we propose the following hypothesis H4:

H4. Job Satisfaction positively affects Individual Performance

2. METHODOLOGY

2.1. Sample and Data Collection Technique

The population of this study is hotel employees in Kota Lombok, with 88 respondents. We use Purposive Sampling where samples are chosen based on our judgment, so it is called judgment sampling. Respondents have been involved in the process of participatory budgeting at least once. We select 3, 4, and 5 star hotels to permit comparative analysis, followingUyar and Bilgin (2011).

In order to increase our response rate, we take three steps suggested byHenri (2006) andYuliansyah, Rammal, and Rose (2016). Those steps are pre-notifications contact, initial distribution of questionnaire, and follow-up. Pre-notification is a telephone call to establish who are the appropriate persons to answer the questionnaire, Initial distribution of the survey instrument is by hand, physically visiting each participating hotel in Lombok City. We issue three or more survey instruments in each hotel to avoid biased results (Lau & Sholihin, 2005), and the last step, and arguably the most important step, is follow-up. We not only collect the questionnaires but also replace the questionnaire if it is said to be lost.

By this approach we generate 108 returns from 200 distributed questionnaires, a very good outcome. Of those collected questionares, 88 are usable, and the others (28) are discarded due to unappropriate responses and incomplete answers.

Table 1 shows the details of the demographic:

2.2. Measurement of Variables

2.2.1. Budgeting Participation

We follow a questionnaire developed byMilani, (1975) modified byStammerjohan et al., (2015). Six questions ask respondents about their contribution to corporate budgeting. They respond on a 5-point Likert scale from 1 (strongly disagree) to 5 (strongly agree).

2.2.2. Pride In Membership

Pride in membership is measured by two questions developed byCable and Turban (2003), and a third “I am proud to be part of an organisation” fromNunnally and Berstein (1994) based onHelm (2013). The 5-point Likert Scale again runs from 1 (strongly disagree) to 5 (strongly agree).

2.2.3. Job Satisfaction

Job satisfaction is understood as an evaluative assessment of job attributes (Fisher, 2000) and the variable measurement uses six questions developed byRiordan, Gatewood, and Bill (1997) and (in our work) based on the job description index (JDX) in the study ofHelm (2013). Indicators of this variable of job satisfaction are (1) the job itself, (2) salary, (3) opportunity for promotion, (4) supervision, and (5) co-workers. The 5 point Likert Scale runs from 1 (deeply unsatisfied) to 5 (strongly satisfied).

2.2.4. Individual performance

Individual performance uses seven questions fromWilliams & Anderson (1991) as usedBurney, Henle, and Widener (2009) andYuliansyah and Khan (2015) among many others. The 5 point Likert Scale runs from 1 (strongly disagree) to 5 (strongly agree).

3. RESEARCH RESULT

In order to test the data, we analyse it using Structural Equation Modelling in particuallary SmartPLS. We choose to use PLS for several factors: small sample size, predictive analysis, and non-normal data (Barclay, Higgins, & Thompson, 1995;Goodhue, Lewis, & Thompson, 2007;Hulland, 1999;Ringle, Sarstedt, & Straub, 2012;Urbach & Ahlemann, 2010). Based on prior studies, applying SmartPLS has two steps: the assessment of the model and the assessment of the structural model.

Reliability Test

Construct reliability is tested by looking for a Cronbach’s Alpha or output composite reliability of more than 0.7.Table 3 below shows construct reliability seen from the value of Cronbach’s Alpha and composite reliability.

Validity Test

Convergent validity is tested by viewing the value of AVE (average variance extracted). Convergent validity is good if the value of AVE is more than 0.5 (Hulland, 1999). InTable 4 below, if a construct has an AVE value of more than 0.50, it can be interpreted as valid.

Discriminant Validity Test

Discriminant validity is measured by looking at the construct value of cross loading and Fornell-Larcker. The discriminant validity is good if the construct value is higher than other constructs.

BP = Budgeting Participation

PIM = Pride in membership

JS = Job Satisfaction

IndPer = Individual Performance

As seen inTable 5 below, the correlation value of construct PA is higher than other constructs. Other indicators similarly correlate higher than their constructs, meaning that each construct has good validity. Moreover, see the correlation square value between construct and AVE value, or the correlation between construct and AVE root.

| BP | PIM | JS | IndPer | |

| Budgeting Participation | 0.879 | |||

| Pride in membership | 0.532 | 0.893 | ||

| Job Satisfaction | 0.575 | 0.750 | 0.736 | |

| Individual Performance | 0.465 | 0.578 | 0.651 | 0.763 |

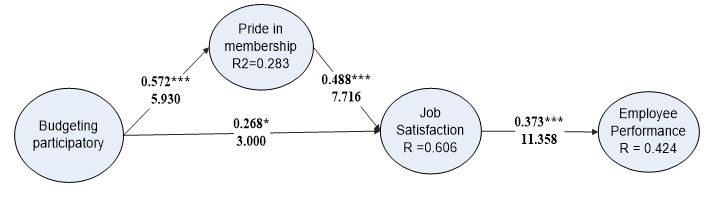

Table 5 above shows that the maximum correlation of Budgeting Participation construct with other constructs is 0.879, while maximum correlation of Pride in Membership is 0.893, Job Satisfaction is 0.736, and Individual Performance is 0.763. Each construct is valid.

3.1. Model Structure Measurement

Model structure is measured by R2value of dependent variable and path coefficient. The relationship within constructs is considered strong when the path coefficient is more than 0.100 and the relationship within variables is considered quite significant if it is more than 0.050 (Urbach & Ahlemann, 2010). The Path coefficient test is done by using a bootstrap procedure with 500 replacements.

*** Significant at 1% (very Significant )

** Significant at 5%

* Significant at 10% (weak)

H1: Budgeting Participation positively affects Pride in Membership

Table 6 shows a positive effect on pride in membership with a very significant value (β= 0.532, t= 7.716, p< 0.01) because t statistics value is above the critical value which is 2.303. Therefore, H1 can be accepted.

H2: Pride in Membership positively affects Job Satisfaction

As seen onTable 6 below, pride in membership positively affects Job Satisfaction with a very significant value which is (β= 0.620, t= 5.930), p< 0.01). It can be seen from t statistics value above critical value which is 2.303. Therefore, based on the result of analysis, H2 can be accepted.

Explanation:

*** Significant at 1% (very significant )

** Significant at 5%

* Significant at 10% (weak)

H3: Budgeting Participation positively affects Job Satisfaction

As seen inTable 6 above, Budgeting Participation positively affects Job Satisfaction with a very significant value which is (β= 0.245, t= 3.000), p< 0.01). It can be seen from the statistics to be above the critical value which is 2.303. Therefore, based on the result of analysis, H3 can be accepted.

H4: Job Satisfaction positively affects Individual Performance

As seen inTable 6 above, Job Satisfaction positively affects Individual performance with a very significant value which is (β= 0.651, t= 11.358), p< 0.01). It can be seen from t statistic value above the critical value which is 2.303. Therefore, based on the result of analysis, H4 can be accepted.

DISCUSSION AND CONCLUSIONS

The aim of the study is to investigate the extent to which participation in budgeting boosts individual performance. Prior research suggests that due to conflicting results, the relationship betweeen budgetary participation and job performance is unclear.Yuen (2007) suggests that it needs another variable, accurately to test the relationship. We predict not only that an individual’s involvement in budgetary participation increases their pride as a member of the organisation but also that the process of budgeting creates a sense of belonging and increases Job Satisfaction. In addition, some studies argue that job satisfaction is crucial to excellent performance. Moreover, If employees are to cooperate to achieve a company’s target, the company must foster corporate pride in each employee.

In order to test our assumption, we do a study in the hotel industry in Lombok City. Our 88 valid replies are tested using SmartPLS 3.0. The result of the study confirms that Budgeting Participation can increase Individual Performance, fully mediated by Pride in Membership and Job Satisfaction. This result means that when individuals become involved in budgeting decision-making, there is an increase of individual pride as a member of the organisation. Similarly, when an individual is valued by an organisation which opens communication channels at all levels, higher job satisfaction triggers irmproved performance.

This study establishes that to involve employees in the process of budgeting increases Individual performance. The company that gives bigger rewards to employees – not just money, but proud feelings and self-esteem will reap its own rewards from the desire of employees to serve the company. Finally, superiors should welcome an individual involvement in decision making in order to leverage each individual’s sense of belonging to an organisation that deserves excellent job performance.

There is no research without any limitation. Our limitations are (1) sampling the hotels of only the city of Lombok may not describe the real condition of the hotel industry elsewhere, and (2) the mediating variables used in this study (Pride in Membership, and Job Satisfaction), may not be the only mediators of individual performance.