1. INTRODUCTION

The transition to an economy based mainly on intangible assets allowed the emergence of scientific research fields as intellectual capital (IC). Over the last decades numerous studies have been conducted in search for methodologies to improve IC management mainly in the business area where the research was more intense and pioneer and where the first and most popular models appeared. The research in public sector did not verify the same intensity and persistence and consequently this area had less attention from researchers. In literature it is possible to realize that even though there are some studies that analyse the management of IC in the public sector, only a limited number propose methodologies specific to this sector. In this context, stands out the work of Cinca et al. (2001), Queiroz et al. (2001;2005), Queiroz (2003;2006) and Verdún et al. (2011) that suggest models and some indicators of IC management designed to public sector.

Although the theory is less developed in public sector, it does not mean that IC is less relevant and several arguments justify the application of the theory to this sector. In fact, the intangibility underlying the concept of IC is present in daily life of public organizations as well as in its objectives (mainly of social nature), output (mostly services) and resources (such as knowledge). However, the application of IC theory has differences in the business and public environment. It is necessary to consider that in private and public sectors the organizations may have different objectives and there are also differences in IC components, in addition to other particularities that are not comparable. Thus, this paper intends, through critical review of literature, to contribute to the discussion of the main aspects about the applicability of IC theory to public sector and to suggest a taxonomy of intangible assets appropriate to this sector. The paper is organized as follows. The next section introduces theoretical background of IC and discusses the main aspects about the applicability of theory to public sector. The third section presents some studies on IC in this sector. The fourth section presents a classification of intangible assets relevant to public sector. And the last one presents main conclusions.

2. DEVELOPMENT OF IC THEORY AND APPLICABILITY TO THE PUBLIC SECTOR

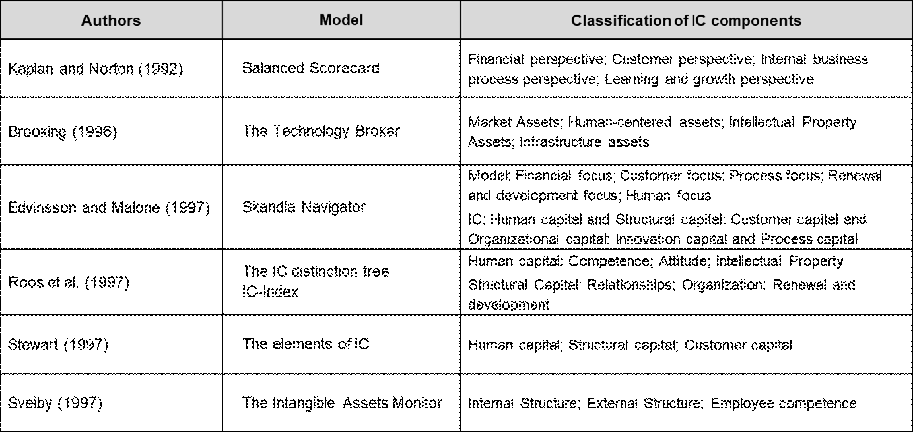

The modern IC theory and the most intense development of research happened on the 1990s of the last century. The concept of IC was popularized with the scientific texts, studies and books published mainly of Kaplan and Norton (1992), Brooking (1996), Edvinsson and Malone (1997), Roos et al. (1997), Stewart (1997) and Sveiby (1997). The recognition that IC creates value and competitive advantages to organizations attracted an increasing interest for the topic.

The concept has many definitions and interpretations that derive from different approaches of business-related disciplines such as strategic management, human resources, economics, accounting and finance. The World Intellectual Capital/Assets Initiative (WICI, 2016:14) presents a very complete definition: “Intellectual Capital encompasses the internal (competencies, skills, leadership, procedures, know-how, etc.) and external (image, brands, alliances, customer satisfaction, etc.) intangibles which are dynamically inter-related and available to an organization, thereby enabling it to transform a set of tangible, financial and human resources into a system capable of pursuing sustainable value creation.” IC concept is frequently understood, as is in this definition, equivalent to intangibles or non-physical resources and is often defined as a set of intangible assets1 , including those that are not reflected into the current financial statements. According to Zambon et al. (2020:13) the concept of IC embodies a subset of unaccounted intangibles usefully employed in the activities of an organization. The terms IC and intangible assets have been associated and widely used in literature, the first more acceptable in management area, and the second if the approach is accounting (Zambon et al., 2020:21) (Verdún et al., 2011:2). Since, it is not an aim of this review to discuss differences in these and others similar concepts that appear in literature, this paper used indistinctly the terms considering intangible assets as IC elements.

IC is commonly categorized in human, structural and relational capital, a traditional tripartite classification. Table 1 presents a comparison of classifications suggested by some of the most popular models of IC management.

IC theory became popular in the private sector, being less developed in the public sector (Joia, 2009:1384) (Meirelles et al., 2017:89). However, any executive in the private or public sector manages intangible assets and recognizes its importance for managing and making better decisions even though, with some exceptions, these are not included in their accounts and financial statements (Queiroz et al., 2005:212). Contrary to the interest that the private sector has shown in the identification and valuation of intangible assets, which includes the elaboration of “IC balance sheets” as an attachment that goes along with the annual accounts, the public sector has made less effort in this regard (Cinca et al., 2001:4) (Queiroz et al., 2005:215). To Cinca et al. (2001:20) regardless of the importance of financial information, the public sector represents an ideal framework for the application of ideas underlying IC theory, arguing that a good management of intangible assets can help public sector institutions to achieve its objectives.

At the public sector level, managers regularly have to make decisions involving intangible assets (ex. a global event where benefits such as image are difficult to quantify; the introduction of information technology in public services where benefits such as citizen satisfaction are difficult to measure), which require large investment volumes and whose benefits are not fully perceived or possible to be measured (Cinca et al., 2001:4). Despite this, public organizations realize the importance of identifying intangible assets in order to make better decisions and show the public the quality of their management processes (Cinca et al., 2001:5). According to Cinca et al. (2001:6), Queiroz (2006:6) and Queiroz et al. (2001:3;2005:217) intangibility is an aspect with high presence in the public sector, so the application of IC theory to this sector must consider its differences in relation to the private sector. The following are some aspects discussed by Cinca et al. (2001), Queiroz et al. (2001;2005), Queiroz (2003;2006), Marques (2005), Wall (2005) and Joia (2009) that justify the applicability of IC theory to public sector.

1- Intangible objectives

In the private sector intangible assets are used mainly to achieve objectives of profitability and of value creation to shareholders (Queiroz et al., 2005:224). Differently, the public sector has essentially intangible objectives, many of a non-financial nature such as national security, administration of justice, raise the general level of culture, seeking to offer quality services (Queiroz, 2003:159;2006:7) (Queiroz et al., 2005:217) (Marques, 2005:440). The achievement of this diversity of objectives can often not be measured in a quantitative way (Wall, 2005:293), and therefore, indicators such as stock prices or the analysis of financial ratios, may have limited use in this situation (Cinca et al., 2001:6) (Queiroz et al., 2005:217) (Queiroz, 2006:7). Thus, the theory of IC allows proposing alternative indicators to measure the degree of fulfilment of the objectives of a public organization.

2- Intangible output

Wall (2005:294) considers that public sector organizations have always used their resources to achieve mainly intangible results. Although the public sector sometimes produces tangible goods, such as roads, the final product of public administrations is mostly services, which are essentially intangible in nature (Queiroz et al., 2005:217) (Cinca et al., 2001:6) (Queiroz, 2003:160) (Marques, 2005:446). For the valuation of tangible goods, costing systems are developed that allow knowing the productivity, analysing the cost-benefit, managing stocks, controlling the quality of the product or the manufacturing processes. When valuing services, many of the concepts developed for physical assets are not applicable, and quality indicators are crucial in this field. Even quality controls take different forms for tangible goods and services, implying in this second case the application of specific procedures such as surveys to measure the degree of satisfaction (Queiroz et al., 2005:218) (Cinca et al., 2001:6) (Queiroz, 2003:160;2006:8). This characteristic supports the application of the theory.

3- Intangible resources

The production factors traditionally considered such as raw materials, machinery, capital, human resources and, knowledge, had preferential uses according to the epochs and sectors concerned, the first three being classified as tangible and the last two as intangible assets (Queiroz et al., 2005:218). If machinery was decisive for industrial companies and capital for the financial companies, then more recently for knowledge-based organizations, is preponderant the intensive use of knowledge in which human resources and ICTs play a central role. In the Public Sector, intangible resources such as knowledge and human resources play a more important role and raw materials, machinery and capital play a less prominent role (Cinca et al., 2001:6) (Queiroz et al., 2005:218) (Queiroz, 2003:160; 2006:8). To Wall (2005:294) public sector organizations have traditionally been, although the gap has narrowed, more intensive in human capital. Queiroz et al. (2005:218) consider that many public administrations fall into the category of knowledge-based organizations, something that will be accentuated with the development of e-government. This circumstance also favours the application of the theory.

4- Internal management tool/Lower urgency in quantifying

The usefulness of intangible assets in the internal management of organizations is related to the decision making of managers, with different perspectives for private companies and public organizations. In private companies, intangible assets serve to earn money in which its monetary quantification is important especially in situations of sale or alienation, whereas in the public sector the issue of quantification is not the only one that is prominent and demanding, which facilitates the implementation of IC theory (Queiroz et al., 2005:219) (Marques, 2005:446) (Queiroz, 2006:8).

5- External presentation and transparency

Public organizations seek to report their activities to citizens about the functions they perform in which, in addition to data on compliance with legalities, budget execution and economic, efficiency and effectiveness indicators, it becomes also important from the perspective of IC, to present information on efforts to optimize the rationality of internal organization, how to develop human resources, how to improve its image, how to improve social well-being and the environment, among others (Queiroz, 2003:161;2006:8). For Queiroz et al. (2005:219-220) if at the business level, IC is considered more as an internal management tool, in the public sector it would be necessary to regulate and control the presentation of documents on intangibles to avoid ruinous investments or unnecessary waste. They consider that transparency in the publication of information by public administrations should be considered a true intangible asset for these entities.

6- Social and environmental responsibility

Queiroz et al. (2005:220) refer that many companies see this responsibility as an expense but also as intangible assets that improve their image, and often publish information about the repercussions of their actions on society and environment in documents attached to the annual accounts. In the case of public organizations the requirement must be higher, this commitment must not be considered merely as something that will improve their image and should be part of its objectives (Queiroz,2003:160;2006:7).

7- Low incentive to adopt new management techniques

Joia (2009:1384) indicates as an obstacle to the implementation of IC projects in public administration the low motivation for adopting new management practices in this environment. It is common for public sector management to slowly adopt innovations of the private sector, in which the latter in a struggle for survival and when operating in a competitive environment needs to quickly adopt the best management practices (Queiroz et al., 2005:220) (Queiroz, 2003:159). Queiroz et al. (2005:221) refers that public sector has been more averse to innovation and that this lack of stimulus is a negative factor that does not favour the adoption of new management techniques, which also occurred with the analysis of intangible assets. These authors refer that the public sector is slower to adopt the measurement and registration of intangible assets, due to the situation of natural monopoly and lack of competition from some organizations, which is not the best way to stimulate its development. To Queiroz et al. (2005:221) and Queiroz (2006:7) the modern management of the public sector has as its flag the attention to the public and the quality of services, which justifies a reflexion on the possibilities of IC.

8- Lower room for manoeuvre of manager

Queiroz et al. (2005:221) and Queiroz (2006:8) refer that although the ideas underlying IC are attractive for application in public organizations, they recognize that its implementation is difficult. This situation is due to the fact that managers are subject to rules and bureaucratic and rigid procedures that hinder their room for manoeuvre, being subject to higher control and demand for transparency in management (Queiroz et al., 2005:221) (Queiroz, 2006:8). Joia (2009:1384) also indicates as an obstacle to the implementation of IC management projects in public administration the little room for manoeuvre to which public managers are subjected.

The use and application of IC theory has differences in business and public environment. According to Queiroz et al. (2005:224) although many ideas proposed in the models developed for private companies can be used to implement in the public sector, not all aspects are in fact comparable. One first aspect concerns with the valuation of intangible assets. Cinca et al. (2001:7) consider that while companies are interested in the monetary quantification of these factors, something indispensable in situations such as sales and mergers, a manager in the public sector may not be as interested in the monetary value of an intangible asset, but more in its rational use. Another aspect is that many models applied in the business sector explain IC concept based on the difference between a company's market value and its book value, something that is not easily translated into the public sector. Indeed, public organizations do not have a market value to allow the calculation of IC value (Joia, 2009:1385). Cinca et al. (2001:8) and Queiroz et al. (2001:7; 2005:224) explain that in this logic it does not make sense to calculate the market value of a city council or a police service. Market value is not the only concept that is hardly applicable in the public area, some accounting concepts may have no meaning or mean something different in the public context such as net income, working capital, brands, customers, among others (Queiroz et al., 2005:224). For example, concerning the concept of brands, in public sector it makes more sense to talk about image or reputation, an important intangible asset to attract investments to a city, university, hospital, etc. which will in turn help to fulfil the organization's objectives (Cinca et al., 2001:8) (Queiroz et al. 2005:225).

In addition to these accounting issues, Cinca et al. (2001:8) and Queiroz et al. (2005:224) argue that must be considered differences in the meaning of IC components in private and public sectors. The category of customer capital does not have the same meaning in public sector given the lack of competition and choice option of citizens (Cinca et al., 2001:8). Therefore, instead of indicators such as the percentage of customers retained or sales from new customers it will make more sense for example to obtain a citizen satisfaction index (Queiroz et al., 2005:224). In the category of organizational capital, Queiroz et al. (2005:225) highlight aspects such as administrative processes and innovation. In relation to the first, it is necessary to consider the different organizational culture in public sector, which is based on a less flexible system towards change, a bureaucratic administration, where administrative processes are very controlled and, where transparency in management is fundamental (Cinca et al., 2001:8) (Queiroz et al., 2005:225). As for innovation, in public sector this role and responsibility is often attributed to universities or research centres (Queiroz et al., 2005:225). With regard to human capital, the public sector also presents particularities, both in the way of attracting employees and in human resources management in general (Queiroz et al., 2005:225). Queiroz et al. (2005:225) also mention that almost all models highlight the importance of human capital, considering people as the basis for generating other types of IC, a philosophy that comes in line with the importance that employees have in public organizations.

Despite these differences, many of the contributions and indicators proposed in the private sector are of relevance to public sector (Cinca et al., 2001:8) (Queiroz et al., 2005:225). However, the design of methodologies for measuring and managing IC elements in public sector organizations enables a more complete and systematic view of its reality.

3. STUDIES ON THE MANAGEMENT OF IC IN THE PUBLIC SECTOR

Over the last decades numerous studies have been conducted in search for methodologies to improve IC management. In literature it is possible to realize that most methodologies that were developed to manage IC appeared in the business area. The research at public sector level did not verify the same persistence and determination. Despite this, it is possible to see that the first examples of studies in public sector were made by applying some of the pioneering methodologies. Joia (2009:1385) presents the examples of: Sveiby (1997) who applied IC theory in the Department of Social Assistance in Adelaide, Australia; and Dragonetti and Roos (1998) that analysed AusIndustry - public agency associated with the Australian Department of Industry, Science and Tourism. Cinca et al. (2001:7) mentions, as an example, the Balanced Scorecard model by Kaplan & Norton (1992) that was used in a pioneering way in the management of Charlotte City, USA. Queiroz et al. (2001:10) refers that the Balanced Scorecard was applied in Spain in the pilot experience of the Barcelona Public Road Actuation Sector; and the Business Navigator, whose initial application was done in the Skandia Insurance Company, was adapted by Edvisson and Stenfelt (1999) to the public sector developing the concept of National IC as a source of wealth creation in countries. Another example was Bontis (2004:15) that developed a national index of IC for the Arabian region using the “IC-navigator”, a version modified of “Skandia Navigator” of Edvinsson and Malone (1997) adapted to nations.

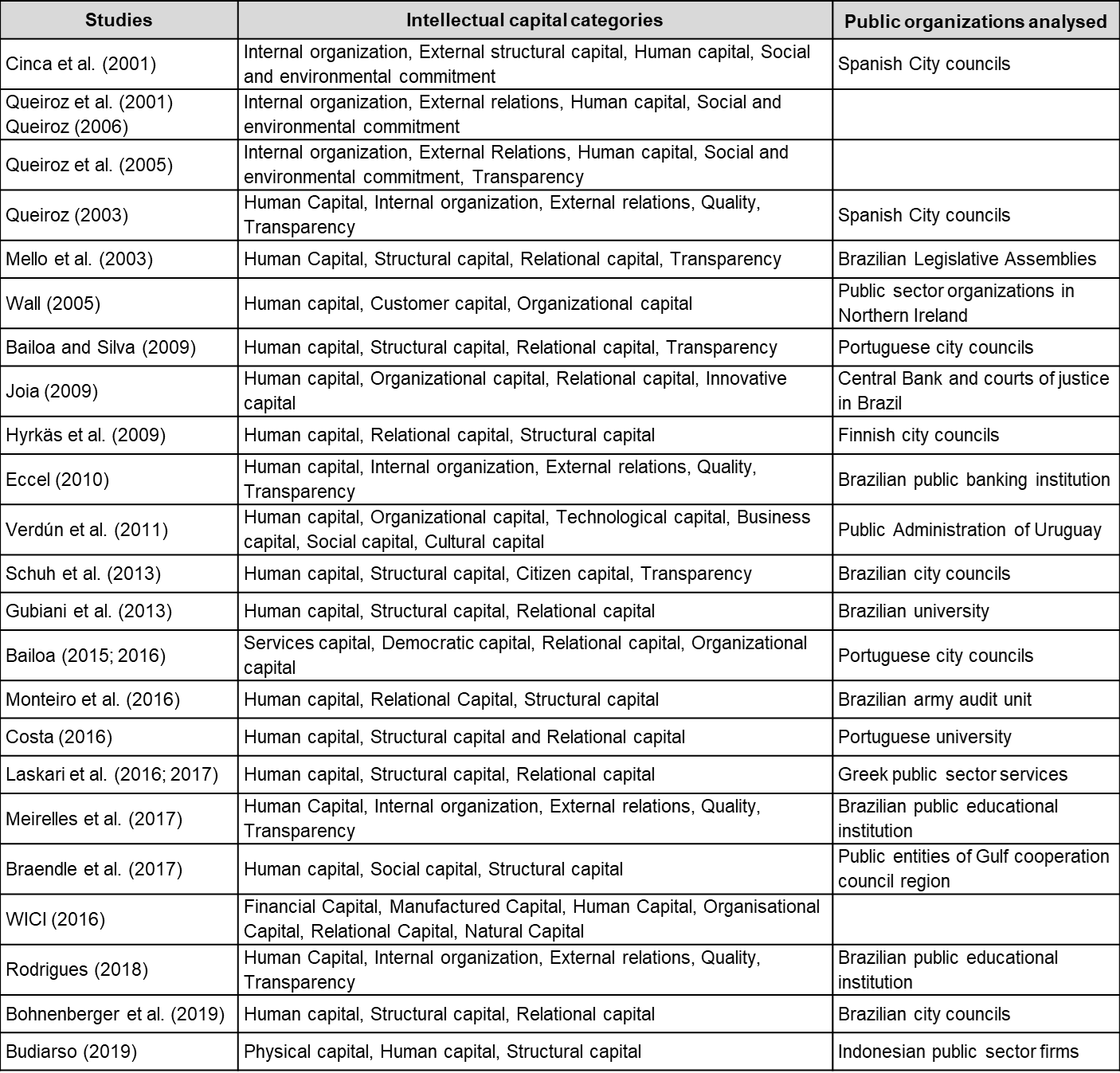

This application was not entirely direct and these methodologies had to be adapted to the analysed reality, since they were not designed directly for the public sector. Thus, it is recognized that this application cannot be done without objections and difficulties (Cinca et al. (2001:7). In fact, it is necessary to consider that in private and public sectors the organizations have different objectives and therefore there are differences in the IC components that can be considered on the methodologies. Over the past few decades there have been some studies that try to overcome these problems of applicability of the theory. In general, studies try to identify dimensions of IC (human, structural, relational, organizational, among other categories) important for a better management of public organizations.Table 2 present some studies that analyses IC in public sector and the dimensions that were considered to describe IC.

Analysingtable 2, it can be seen that the dimensions most studied are human, structural and relational capital, that is, the traditional tripartite classification of IC. The emphasis on human capital shows the importance that the availability of qualified employees, with adequate training and integrated into a favourable work environment, is an essential condition for organizations to achieve their goals. The assets of structural capital include work procedures, accumulated knowledge, ways of approaching problems, structural organization, the level of internal bureaucracy, the ability to work in groups, information systems, among others, which represent the organization's work processes and objects essential to improving the quality of services offered to the public. The assets of relational capital include the entity's relations with citizens in general, users of services, suppliers, companies, government entities, collaborations, agreements and alliances, and also the image, reputation, public recognition and the organization's credibility, which are valued by society and fundamental for the organization to increase capital flows and development opportunities.

In addition to these assets, appear in some studies other dimensions that have not been included in the existing models developed for private companies and considered decisive in the management of public organizations, such as social and environmental aspects, transparency and quality, although with less focus than the other dimensions in the various analyses. The dimensions that refer to social and environmental commitments include the set of actions that organizations implement both to improve the well-being of the population and to favour the environment, in order to provide a better quality of life and development. The transparency dimension include the set of actions related to the publication and disclosure of information in order to make possible to inform citizens about governmental action and, also, a higher control of public management, fundamental aspects for the reduction of corruption situations in the management of public funds, in order to allow a major participation of citizens in government decisions and activities. The quality dimension is fundamental for the development of the main activity of public sector organizations, which consists mostly in the provision of services. Therefore, the improvement of quality of services shows the concern of organizations with the satisfaction of citizens and is perceived by their participation in public services.

Among the presented studies, it was possible to find models for management of IC in the public sector as the models of Cinca et al. (2001), Queiroz et al. (2001;2005), Queiroz (2003;2006) and Verdún et al. (2011). These models present classifications of intangible assets and suggest some indicators of IC management especially for public organizations. Cinca et al. (2001:9), Queiroz et al. (2001:7) and Queiroz (2006:10) classify IC in four categories: internal organization, external relations, human capital, social and environmental commitment. Queiroz et al. (2005:230) also propose a model with similar dimensions of the last referred but classifying IC in five dimensions adding the category of transparency. For each category, intangible assets are defined and, to quantify them, some indicators are suggested. Queiroz et al. (2005:229) refer that this procedure is not free from difficulties, since the indicators have practical limitations because they can present a partial or distorted image of the organization, especially when using indicators that try to quantify intangible concepts. As the public sector can include organizations such as municipalities, universities, firefighters, hospitals, etc., each entity can adapt the scheme, which is considered as a generic guide, and needs to select and adapt the appropriate indicators (Queiroz et al.,2001:9;2005:230). Another study to be mentioned is that of Verdún et al. (2011) which classify IC elements into six categories: human, organizational, technological, business, social and cultural capital. As in the models mentioned above, to each category a set of indicators relevant were selected.

In another study Queiroz (2003:209) classifies IC elements into five categories that include the three traditional dimensions of IC (human, structural and relational capital) and highlights two more groups of intangibles: quality and transparency. The model has two main parts that resemble a traditional balance sheet, with an intellectual asset and an intellectual liability in which are registered the positive attitudes or actions that may contribute to increase IC and the negative ones that may generate an intellectual liability (Queiroz, 2003:214). Queiroz's model (2003) was the methodological reference for the studies of Mello et al. (2003), Bailoa and Silva (2009), Eccel (2010), Meirelles et al. (2017) and Rodrigues (2018).

Research exposed on table 2 presents some diversity both in the methodologies used, either the organizations studied that in the case of public sector can be organizations of different types. The diversity and exploratory nature of studies brings difficulties in generalizing or confirms the results and to adopt general implications (Chen, 2011:3597) (Liu, 2013:128). In fact, the dimensions in which IC is subdivided not always converge, and in each situation are adjusted for cases studied. Chen (2011:3593) after conducting a series of studies refers that the concept got different dimensions when applied to different industries.

4. THE INTANGIBLE ASSETS OF RELEVANCE TO PUBLIC SECTOR

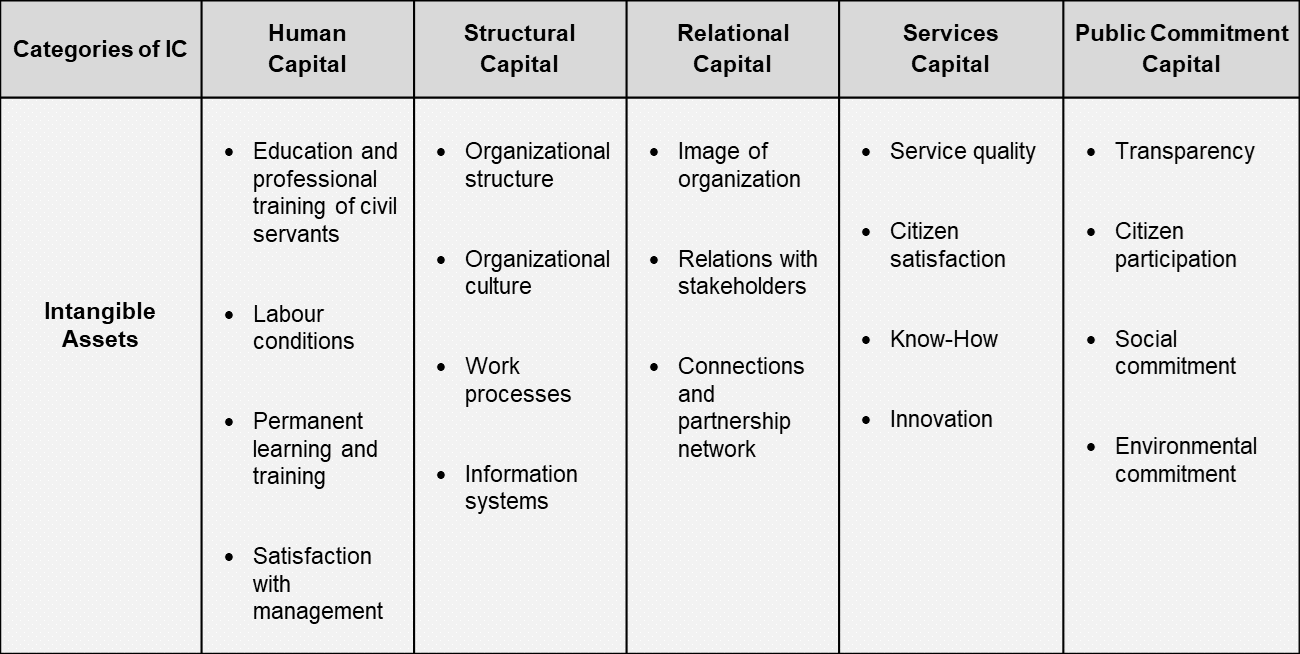

The last sections analysed the state of art on the management of IC in public sector. Based on the main contributions of literature this section intends to define the intangible assets appropriate to public sector organizations, since one of the objectives of this paper is to suggest a possible taxonomy. Cinca et al. (2001:8) and Queiroz et al. (2005:224) argue that a management model for the public sector that includes indicators of intangible assets should help to show the importance of these to achieve the objectives of the institution. The model should highlight how intangible assets are used to improve the quality of services offered to the public, must show the relevance in achieving excellence in management and, it must reflect the institution's commitment to social and environmental development (Cinca et al., 2001:8) (Queiroz et al.,2001:6;2005:224). Thus, following these recommendations, the set of categories of IC considered relevant to public sector were (table 3): Human capital, Structural capital, Relational capital, Services capital and Public Commitment capital.

The first three categories correspond to the traditional tripartite classification of IC. Human Capital encompasses human resources, their knowledge, abilities and attitudes, including as intangible assets: Education and professional training of civil servants; Labour conditions (the work environment, safety, possibilities of promotions, and incentives); Permanent training and learning; and Satisfaction with management. Structural Capital includes the processes, procedures and working methods that enable the organization to function and includes: Organizational structure; Organizational culture; Work processes; and Information systems. Relational Capital represents the organization relations with several players in its external environment, and includes as assets: Relations with stakeholders (suppliers, government agencies, investors, associations and other institutions); Connections and partnership network (partnerships, collaborative projects, cooperation networks and other agreements and alliances); and the Image of organization (marketing, social networks, promotion and participation in events).

Services Capital is not presented as a main category in other models despite the final product of public sector being mostly services. The category of Services capital is considered because the provision of public services is a key objective of public organizations and therefore of public administration. Thus, this category includes as intangible assets: Service quality; Citizen satisfaction; Know-How; Innovation. The category of Public Commitment Capital also does not appear in other models, and is justified by the very nature of public organizations and their objectives for improving social well-being that are expressed by a commitment with society. Thus, this category includes the commitments of: Transparency (to improve accountability, credibility and transparency trough the disclosure of information and its accessibility as the publication of budgets and accounts reports, legislation, meetings minutes, etc.); Citizen participation (to improve dialogue, relationship and participation of citizen as the possibility of making suggestions and complaints, surveys, newsletters, among others); the Social commitment (which refers to the measures taken by public organizations in the social sphere, therefore, to improve the well-being of the population); and, the Environmental commitment (the measures taken in order to safeguard and favour the environment).

To each category it is suggested the definition of indicators to represent and quantify the diverse intangible assets. Each organization must incorporate those indicators that consider appropriate in accordance with its objectives and strategies. It is also suggested to quantify the organization level of IC and for that it can be used a scoring system to produce an indicator or a performance index of IC that could allow monitoring the evolution of the development of the organization IC and therefore contribute to its management and decision support.

5. CONCLUSION

The topic addressed in this paper intended to be a reflexion about the management of IC in public sector. To fulfil first objective the main aspects about the applicability of IC theory to this sector were discussed. It was possible to realize that IC theory became popular and intense in the private sector but research in public sector did not verify the same intensity lying less developed. However, on literature it was possible to find several arguments that justify the application of the theory to public sector namely, the fact that intangibility underlying the IC concept is present on the objectives, output produced and resources used by these organizations; the need for transparency; the higher demand for social and environmental responsibility; despite difficulties in this application, such as less incentive for the adoption of new management techniques and less room for manoeuvre of manager, among other justifications. Despite the application of IC theory has differences in the private and public sector, many ideas proposed on business area can be useful to public sector but there are aspects that are not comparable. The need to adapt the methodologies was also highlighted, since the models developed in the business environment and some concepts that were designed specifically for private companies are difficult to apply in the public area.

This work also presented some studies that try to overcome these problems of applicability of the theory. In general, studies try to identify categories of IC important for a better management of public organizations. The dimensions that stand out in most studies were human, structural and relational capital, that is, the traditional tripartite classification of theories in this area. Nevertheless, other dimensions related to aspects considered critical in the management of public organizations, such as social and environmental responsibility, transparency and quality, emerged, although in a smaller number of studies.

In the specialized literature it is possible to find a multiplicity of methodologies developed to the management of IC in business sector. However, it was also possible to find the application of IC concept to the public sector management and yet, other research paths, as on the territories management and on digital networks management. Nevertheless, the diversity and exploratory nature of studies brings difficulties in generalizing the results and the dimensions in which IC is subdivided not always converge, and in each case are adjusted for cases studied. The diversity of methodologies is justified by the fact that in each area in which the research takes place (business, public sector, territories, digital networks) there is a specific set of intangible assets that are decisive to achieve the objectives of the organizations concerned.

Thus, based on the main contributions in the literature, this paper also suggested a classification of intangible assets appropriate to public sector. The IC categories were defined based on the importance and role of the diverse intangible assets to achieve the objectives and mission of public organizations. The set of categories considered were: Human capital, Structural capital, Relational capital, Services capital and Public Commitment capital. The classification presents two categories that don’t appear as main categories in other models. In one hand, the Services capital, because the final product of public sector are mostly the provision of public services. On the other hand, the Public Commitment capital, that is justified by the very nature of public organizations objectives which intends improving social well-being that are expressed by a commitment with society in terms of transparency, citizen participation and, social and environmental commitment.

The models and studies presented in this paper show that there is a line of investigation that confirms the relevance of IC in the public sector, allowing recognizing the importance that intangible assets have for the strategic management of public organizations. This reflexion allows concluding that the strategic management of intangible assets in organizations of public sector is just as on private sector a source to obtain sustained competitive advantages. The appropriate use of intangible assets allowed by an adequate management methodology contributes to create value. So, it is expected that this work could contribute to the research of methodologies to improve IC management in public sector.