1. INTRODUCTION

Profitability performance indicators measure a company’s effectiveness and successfulness. Typical indicators used as company profitability measures are return on equity (ROE) and return on assets (ROA); in addition, return on investment (ROI) can also be used. Capital structure, i.e. debtequity mix is one of the most important financial choices that every management may take. It has significant impact on companies’ financial performance and corporate value. Management should stream towards optimal capital structure that minimizes capital costs and maximizes company value. By optimizing the financial and capital leverage management may achieve optimal capital structure. Recent research on capital structure has focused on trade-off and pecking order theory. The trade-off theory encompasses optimal capital structure by trading off the tax benefits and costs of agency problems, while pecking order theory proposes that capital structure choice is guided by asymmetric information. The basis for trade-off theory and capital structure associated with the value of the company was defined byModigliani and Miller (1958). In their work they demonstrated the irrelevance of capital structure on the company value. Assumptions of irrelevance were eligible only in perfect market conditions (free access to the market by all investors, zero transactions cost and no tax difference between dividends and capital gains, and rationality of all players present in the market). In their later communication,Miller and Modigliani (1963) corrected an error from the previous model by considering the effect of taxes and the risk of debt on capital structure. Although they upgraded the first model with this communication and brought theory closer to the real financial environment problems regarding capital structure and corporate value, the model was nevertheless far away from the praxis in the real world. Further research on corporate value and capital structure introduced the agency problem and related agency costs (Jensen and Meckling, 1976) as well as free cash flows problem and its control by debt financing (Jensen, 1986;Stulz, 1990). By encompassing all stated effect and concepts, trade-off theory was developed.

Pecking order theory was developed byMyers and Majluf (1984) by explaining financial behavior of corporation and hierarchy in choosing sources of finance.Myers (1984) upgraded the pecking order by recognizing the cost of financial distress besides asymmetric information. The pecking theory assumes that cost of financing increases with asymmetric information. Usually, corporate managers possess more information than outside creditors and even shareholders, which leads to the tendency of choosing internal sources over external sources. Additionally, when choosing external sources managers prefer debt over equity since they are less expensive.

In addition to these central theories of capital structure, there are authors and studies that have analyzed strategy of competing in the product market and product characteristics and its influence to the capital structure (Titman, 1984;Maksimovic, 1988,1995;Stulz, 1988;Rotemberg and Scharfstein, 1990). Beside the industrial-organization-based approach, the influence of corporate control on the capital structure was investigated as well (Stulz, 1988;Harris and Raviv, 1991;Mehran, 1992;Zwiebel, 1996;Garvey and Hanka, 1999;Mishra and Mcconaughy, 1999;Novaes, 2003). Besides the core theories that have recognized fundamental factors that influence capital structure, there are wide-ranging theories identifying numerous internal factors and corporate characteristic that are influencing capital structure.Harris and Raviv (1991, p. 336) reviewed the surveyed literature and identified the following internal factors that shape corporate leverage, namely volatility, bankruptcy, profitability, fixed assets, tax shields, R&D, growth opportunities, size, free cash flow, ownership structure.

Due to the importance of this topic, we have decided to investigate the Croatian hotel industry profitability performance under capital structure and other company characteristics. The question that may arise relates to the way of investigating the hotel industry. The main issue and main disadvantage of the Croatian economy and its GDP is that it is highly dependable on tourism since total impact and share of tourism in GDP is 19,7%. With respect to indicated the main purpose of this paper was to present a new insights on profitability performance of the hotel industry in Croatia under capital structure. Besides that, goal and aim of the paper is to bring closer topic on causal relation of financial performance and capital structure as well as other companies characteristics to the experts. Additionally, to raise awareness and to influence to the state of minds of financial manager and decision makers was one of goals. Additionally, in line withČrnigoj and Mramor (2009) who suggested that financial behavior and linked capital structure is somewhat different in Emerging European Countries from those in the developed market economies, we have chosen Croatian hotel industry. It should be highlighted that financial performance is not only dependable on the capital structure.Menicucci (2018) found out that hotel profitability is determined by financial crisis, business model and ownership structure, size, internationalization, location, accommodation. Other authors arrived at the same result associated to the financial crisis and profitability (Shahzad et al., 2015).Xu and Chi (2017) pin pointed operating efficiency U.S hotels to be linked with hotel size and service price.Ben Aissa and Goaied (2016) examined Tunisian hotel profitability and indicated that hotel size has negative impact but also brings to light managerial skills as important factor for hotel profitability. Similar research on leadership styles and human capital (Tran, 2017;Sardo, Serrasqueiro and Alves, 2018) highlighted the positive influence of both human capital and leadership styles on hotel companies’ financial performance.

The paper is structured as follows: Section 1 provides the introduction. Section 2 presents an overview of existing literature on the topic of capital structure in the hotel industry sector and in the emerging markets. Data and methodology used for this analysis is elaborated in Section 3. In Section 4 the main empirical results are presented, while Section 5 provides an overall summary of final conclusions.

2. LITERATURE REVIEW

Frydenberg (2011) concludes that theories of capital structure are not “holy grail”, i.e. they are not providing answer to the everlasting questions of how and what financing politics firms should use. He also states that a search for a model that can explain capital structure is still work-in-progress. Based on that, we point at the majority of studies on capital structure and the impact that they have on profitability which have been investigated in developed markets; however, in the last two decades, the number of studies that have researched this topic in emerging markets are on the rise. Contrary to the main theories developed on mature markets, results from emerging markets research brought new insights on capital structure theory and profitability. Study on capital structure of Hungarian companies carried out byNivorozhkin (2002) revealed that less indebted companies are more profitable than more indebted ones, which goes against the fundamental theories. Furthermore, they discovered negative relationship between leverage and proportion of tangible assets, caused by nonexistence of long-term debt on the market. In addition to the above,Baer and Gray (1995) have previously performed a similar regression analysis on the Polish market and firms, but found out positive yet primarily insignificant coefficients on the same variables. On the same track is a study carried out byČrnigoj and Mramor (2009) who investigated what influences the capital structure choice in Slovenian firms, arriving at the conclusion that financial behavior of emerging countries is somewhat different from those in developed markets.Lucey and Zhang (2011) have investigated the impact of country-level financial integration on corporate financing choices in 24 emerging counties, selected from MSCI Emerging Markets Indices 2007, with China omitted from the sample. Results from the study indicated that higher financial integration leads to significant use of debt and equity financing, which is more emphasized for high-growth firms than low-growth firms on credit use. Correspondingly, large firms in the process of integration tend to use more debt, especially long-term debt, and to issue more equity than small-firms.Booth, Aivazian, and Demirguc-Kunt (2001) analyzed capital structure of firms from ten developing countries and concluded that factors which influence capital structure choice are similar between developed and developing countries. In addition, they drew their attention on the fact that firms in developing countries have higher dependence on short- term debt and trade credit. These results could be explained by the fact of undeveloped financial markets. Limitations regarding outside financing were recognized in the study byKlapper, Sarria-Allende, and Sulla (2002) which investigated SME financing behavior in Eastern Europe.Nivorozhkin (2005) examined capital structure of five EU accession countries (Bulgaria, Czech Republic, Poland, Romania and Estonia). His results pointed out that the capital structures of firms of observed EU accession countries have a steady tendency towards leverage levels of the observed EU countries. Additionally, he found out that tangible assets are a poor source of collateral in five examined EU accessed countries.Abor (2005) brings insight for Ghanaian firms and identifies significant and positive relationship between short-term debt to return on equity and negative relationship of long-term debt.

Berk (2007) studied the role of the Slovenian capital market on determining corporate capital structure; results have indicated that private firms use significantly more debt financing than public ones. Similar results for companies from Serbia, Croatia, Montenegro and Macedonia were obtained byArsov and Naumoski (2016) regarding firm size and leverage. In addition, in their study results indicated negative impact of profitability and tangible assets on leverage. Results of their study partly confirmed previous results of analysis for Serbian companies carried out by several authors (Malinić, Denčić-Mihajlov and Ljubenović, 2013). In their analysis,Malinić, Denčić-Mihajlov, and Ljubenović (2013) obtained results which indicated that leverage decreases with profitability, liquidity, tangibility and cash gap and increases with growth opportunities. To some degree, these results are in line with study ofIlyukhin (2017) in which he examines Russians nonfinancial traded firms. He found that most reliable variables that influence capital structure are firm size, growth opportunity and industry mean.

Croatia is not an island regarding results obtained in papers carried out on capital structure.Klapper and Tzioumis (2008) investigated influence of taxation on the capital structure in Croatia and concluded that results reveal significant impact of corporate taxation on corporate structure. Delic (2016) investigated financing behavior of Croatian SME and confirmed that Myers pecking order was statistically insignificant. Reasons for that may be found in the facts that Croatian financial markets are undeveloped and shallow, bank loans are main source of long-term financing and high insolvency.Učkar (2007) have analyzed relationship of financial structure and stock market values of selected companies form Croatian financial market and got positive results for trade-off theory. In the same vein, the model proposed byUčkar (2007) was not significant for traditional approach, Modigliani-Miller theory and signal theory of financial structure management.Harc (2015) investigated the connection between size and capital structure of 500 Croatian SMEs. Results from the study pointed out that Croatian SMEs tend to use long-term debt. Similar results were obtained byJežovita (2019). Results of the analysis of 111 large Croatian companies carried out byPepur, Ćurak, and Poposki (2016) are in line with previous studies of undeveloped markets (Booth, Aivazian and Demirguc-Kunt, 2001;Klapper, Sarria-Allende and Sulla, 2002;Nivorozhkin, 2002;Črnigoj and Mramor, 2009;Malinić, Denčić-Mihajlov and Ljubenović, 2013). The main result differs from main capital structure theories.

In the past, various authors have examined capital structure of companies from tourism and hotel industry. In study ofShamaileh and Khanfar (2014) reveal positive and significant impact of leverage to ROI. Capital structure of Portuguese hotel firms were examined bySalsa, Matias, and Afonso (2018) and results confirmed that variables examined in modern basic theories are significant. Strongest variable was tangibility; likewise, profitability has negative relationship with indebtedness. Pecking-order theory as well as trade of theory are confirmed. Similar results for Portuguese SME hotel companies were obtained byPacheco and Tavares (2017) but with the indication that examined companies are not homogeneous, and both theories are necessary to explaining their capital structure. Somewhat different results were obtained byKaradeniz et al. (2009) and neither the trade-off nor the pecking order theory exactly seem to explain the capital structure of Turkish hotel companies.Phillips and Sipahioglu (2004) investigated impact of capital structure of quoted organizations with interest in hotel industry on their profitability. Results implied that there is no significant evidence on the relationship between the level of debt and financial performance. Survey of capital structure and impact on the profitability of Indian hotel companies byMadan (2007) indicated that leverage has positive impact just on a few observed companies while others affected negatively.

This study is based on the previous reserch (Burja, 2011;Li, 2012;Berzkalne and Zelgalve, 2014;Shamaileh and Khanfar, 2014;Vătavu, 2015;Oberholzer, 2017;Herzog, 2018).

3. DATA AND METHODOLOGY

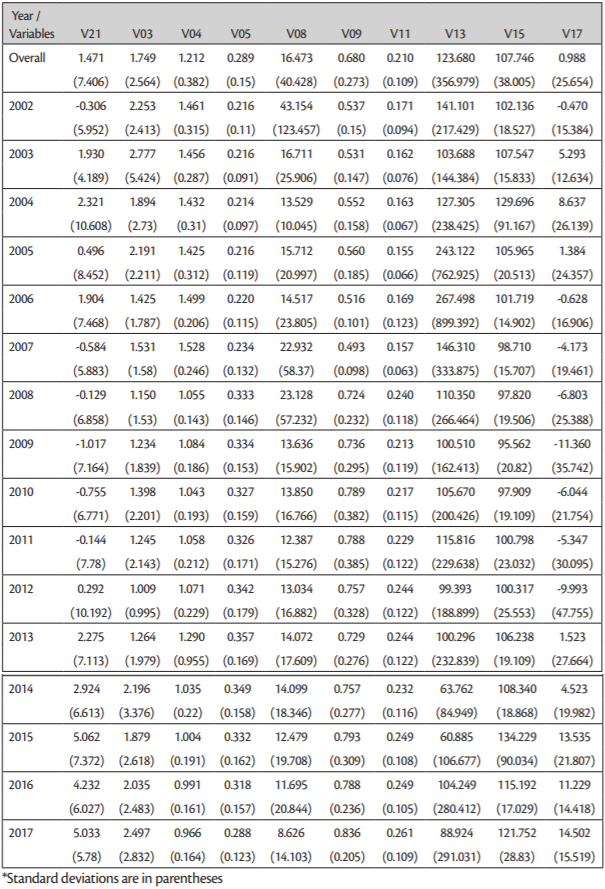

For the purpose of this research, secondary data from Financial Agency (FINA) were used for all Croatian hotel companies listed on the Zagreb stock exchange. The study is based on the 2002- 2017 financial data from a final sample of 20 hotel industry companies. To satisfy the criteria of inclusion in analysis the observed FINA data set of hotel companies for all variables should be viable for the whole period 2002-2017. Although, the number of listed hotel industry companies is 27 in the observed period we have excluded seven companies due to a couple of reasons: lack of data, mergers and acquisition by other company in the observed period, long-term insolvency and bankruptcy, or period of indexation shorter than observed 16 years. We tested various internal variables (Table 1) that influence financial performance of selected Croatian hotel industry companies expressed by proxies i.e. return on equity (ROE) and return on assets. Additionally, it should be highlighted that the spillover of the Global Financial crisis and its impact on the Croatian economy took place longer than in most other countries. The duration of the crisis extended over a six-year period, from 2009-2015.

Source: Autors

All explanatory variables are approximated, measured and presented inTable 2. (see appendix).

Since data are indexed by both unit (hotel company) and time (year), a panel regression model was employed. Several models have been used to select appropriate models. First, an applied two-way fixed effects was used, while random effects panel model was employed afterwards.

In order to evaluate the models, we have tested for serial correlation, contemporaneous correlation, and heteroscedasticity. To address the presence of serial correlation several tests have been used. Woolridge test is not significant even at α = 0.10 (F=0.564, p = 0.462), but Bias-corrected Born and Breitung Q(p) test is significant for most variables (p is mostly less than 0.001). Inoue and Solo LM-test does not show significant correlation (all p > 0,10). Two out of three tests do not reject the null hypothesis of no serial correlation but due to the one significant test, the possibility of autocorrelation could not be ruled out.

For heteroscedasticity testing we have used Modified Wald test; with chi2 = 6213.22, p < 0.001 the null hypothesis of no heteroscedasticity was rejected.

Cross-sectional Independence/Contemporaneous Correlation was tested using several tests, all with the null hypothesis of cross-sectional independence: Pesaran’s test (Pesaran = 0.444, p = 0.6569) is the only test that does not show cross-sectional dependency. Friedman’s test (Friedman = 31.138, p = 0.0390) and Frees’ test (Frees = 1.585) are indicating cross-sectional dependency as well as CD-test which for all except one variable has p < 0.001. Since three out of four tests are significant it is reasonable to reject the hypothesis of cross-sectional independence.

With the heteroscedasticity, contemporaneous correlation and possible serial correlation, it becomes evident that fixed and random models are not proper models to be employed in this case. Appropriate models are those with Panels Corrected Standard Errors (PCSEs) and Driscoll-Kraay standard errors fixed effect models (SCC). Feasible Generalized Least Squares (FGLS) model could not be used since T > N (Hoechle, 2007).

4. EMPIRICAL RESULTS REGARDING VARIABLES THAT HAVE INFLUENCE ON PROFITABILITY PERFORMANCE OF CROATIAN HOTEL INDUSTRY

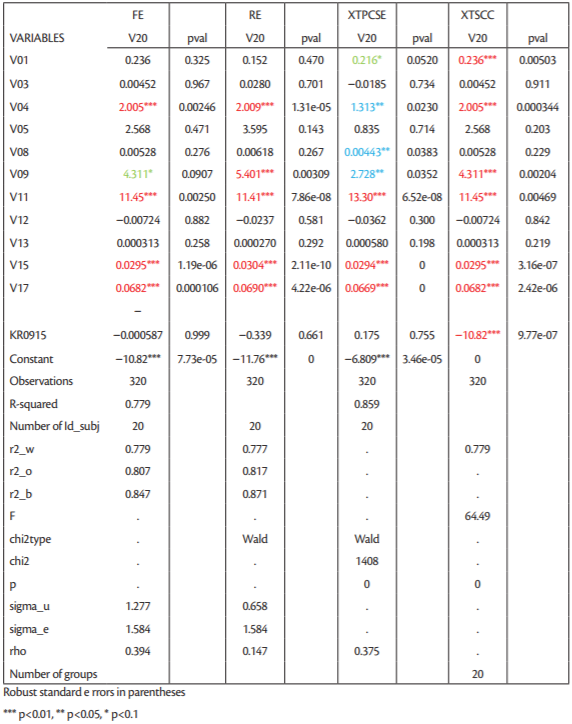

Results for all models – fixed effects, random effects, PCSE and Driscoll-Kraay standard errors fixed effect models (SCC) – are presented in tables3 and4 (see app.). We have observed the influence of internal variables on two main financial performance indicators, ROA and ROE, of the Croatian hotel companies index on the Zagreb stock exchange. Due to the carried out we have excluded fixed effects model as well as random effects models. Appropriate models, such as Panels Corrected Standard Errors (PCSEs) and Driscoll-Kraay, were used. Results presented intable 3 (see app.) reveal that using Panels Corrected Standard Errors (PCSEs) following ratios as significant to ROA cash ratio, financial stability coefficient, indebtedness factor, degree of coverage I, total assets turnover, cost to income ratio and gross profit margin ratio. Driscoll-Kraay standard errors fixed effect suggest that indebtedness factor is not statistically significant but however implies crisis as significant factor. Basically, it may be concluded that there is a strong positive connection between financial stability, indebtedness factor, degree of coverage I, total assets turnover, cost to income ratio, gross profit margin to financial performance indicator - return on assets. Nevertheless, expected crisis had a negative influence on the ROA in the observed period. We have to draw the attention to the following issue, that capital structure observed through the share of shareholder’s equity in fixed assets is significant in all models.

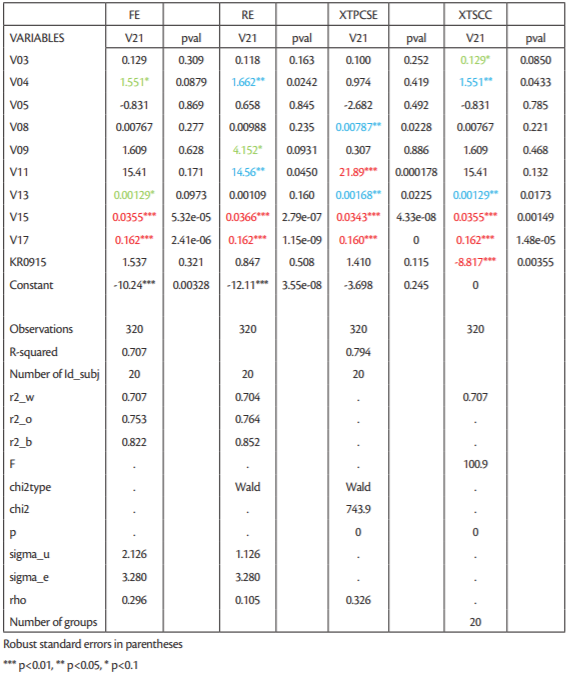

Also, for ROE as the financial performance measure the same test was carried out, thus ruling out fixed effects and random effects models, with results presented intable 4 (see app.). Panels corrected standard Errors (PCSEs) model indicated that indebtedness factor, total assets turnover, accounts receivable turnover, cost to income ratio and gross profit margin have significant impact to return on assets. The highest significance of ROE have total assets turnover, cost to income ratio and gross profit margin, at the same time indebtedness factor and accounts receivables turnover have somewhat lover significance. Total assets turnover has the highest impact.

Unlike the previous model, PCSEs model Driscoll-Kraay revealed slightly different results for indebtedness factor and total assets turnover indicated it as insignificant while it pointed to crisis variable as very significant. Additionally, current ratio and financial stability in this model are significant also. Others analyzed variables were signaled as a very significant. Capital structure observed through share of shareholder’s equity in fixed assets is revealed as insignificant and does not have influence on return on equity among Croatian hotel companies.

5. CONCLUSION

The purpose of this paper was to present new insights on profitability performance of the hotel industry in Croatia by taking into account specific environment and industry issues. The results were obtained by applying dynamic panel methodology and revealed results that run contrary to capital structure. In the PCSEs and Driscoll-Kraay model capital structure was indicated as significant to return on assets while insignificant to the return on equity. Besides capital structure for both financial performance measures ROA and ROE, statistically significant variables were expected cost of income ratio and gross profit margin. We have to highlight that the crisis was indicated by using Driscoll-Kraay model for both measures as significant with high negative impact.

Given the importance of tourism and hotel industry to the Croatian economy, and the results provided by this study, we recommend it to the hotel decision makers. In addition, result may be used by financial managers in the hotel industry companies. The findings bring insights on financial performance measures and significance of examined variable as well as their impact to return on assets and return on equity. In addition, the crisis variable indicate that financial decisions should take into consideration outside economic environment and their impact on the industry and company as well.

This study also contains limitations, which emerge mainly due to a lack of data on growth opportunities, total debts and long term debt variables and specific industry financial elements as occupancy rates and revenue per available room. Although result provided by this research indicate significant impact of some variables on financial performance there is open question of results if some other variables were taken in account like market capitalization and room occupancy and others.

Suggestion for future research would be to include other capital structure variables as growth opportunity size of company, macroeconomics variables, tax shield, legal characteristic, financial market development measures, managerial style etc. It would be interesting for future work to expend current study at the level of entire central and eastern European region and to compare result of different counties.

* This paper has been financially supported by the University of Rijeka, for the project ZP UNIRI 2/17.

* This work has been fully supported by/supported in part by the University of Rijeka under the project number 17.02.2.2.01.